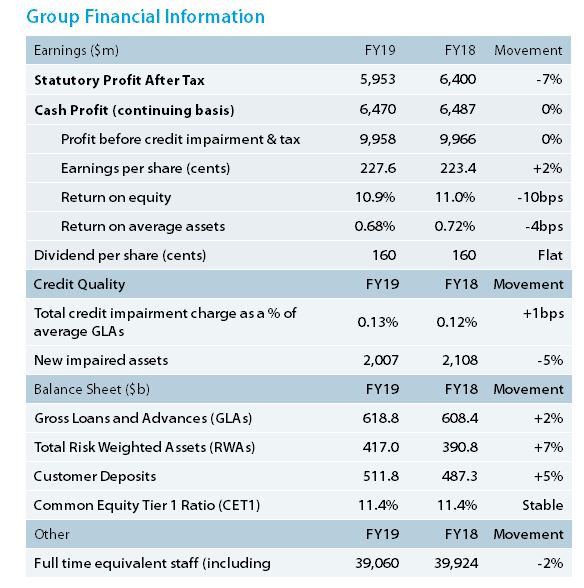

ANZ today announced a Statutory Profit after tax for the Full Year ended 30 September 2019 of $5.95 billion, down 7% on the prior comparable period. Cash Profit[1] for its continuing operations was $6.47 billion, flat with the prior comparable period. Cash Earnings per Share increased 2% to 228 cents.

ANZ’s Common Equity Tier 1 Capital Ratio was stable at 11.4% and around $3.5 billion above the Australian Prudential Regulation Authority’s (APRA) ‘unquestionably strong’ measure. Return on Equity decreased 10 bps to 10.9%.

The proposed Final Dividend is 80 cents per share, partially franked at 70%. This equates to $2.3 billion to be paid to shareholders against ANZ’s market capitalisation of $78 billion.

CEO COMMENTARY

ANZ Chief Executive Officer Shayne Elliott said: “This has been a challenging year of slow economic growth, increased competition, regulatory change and global uncertainty.

“Despite the challenges, we maintained focus on improving customer experience, balance sheet strength and improving our culture and capability. In doing this, we significantly reduced the cost and risk of operating the bank even though strong headwinds impacted the sector. Investment was at record levels and we are a far stronger bank as a result of the progress made this year.

“Retail & Commercial in Australia had a difficult year. Along with increased remediation charges, intense competition and record low interest rates have had a significant impact on earnings. While yet to flow through to the balance sheet, management actions and operational improvements have seen a steady recovery in home loan applications in recent months. This momentum is expected to be maintained into 2020.

“The transformation of Institutional continued to provide prudent and diversified growth. While macro conditions had an impact on financial performance in the second half within Markets, the broader business is now generating returns above our cost of capital, providing important diversification given the lower growth in our home markets.

“New Zealand delivered a solid underlying result in an increasingly competitive environment. Compliance and remediation costs contributed to higher operating expenses. This was mainly driven by the complex work required to comply with new regulatory standards that all subsidiary banks be able to operate as stand-alone entities.

“In proposing the Final Dividend and franking level, the Board considered the bank’s strong capital position and its organic capital generation capacity. Our decision to reduce franking to a new base reflects the changed shape of our business as well as recognising how important the dividend, franking and predictability is to shareholders,” Mr Elliott said.

[1] All financials are on a Cash Profit Continuing Basis with growth rates compared to the Full Year ended 30 September 2018 unless otherwise stated.

{kind=link}