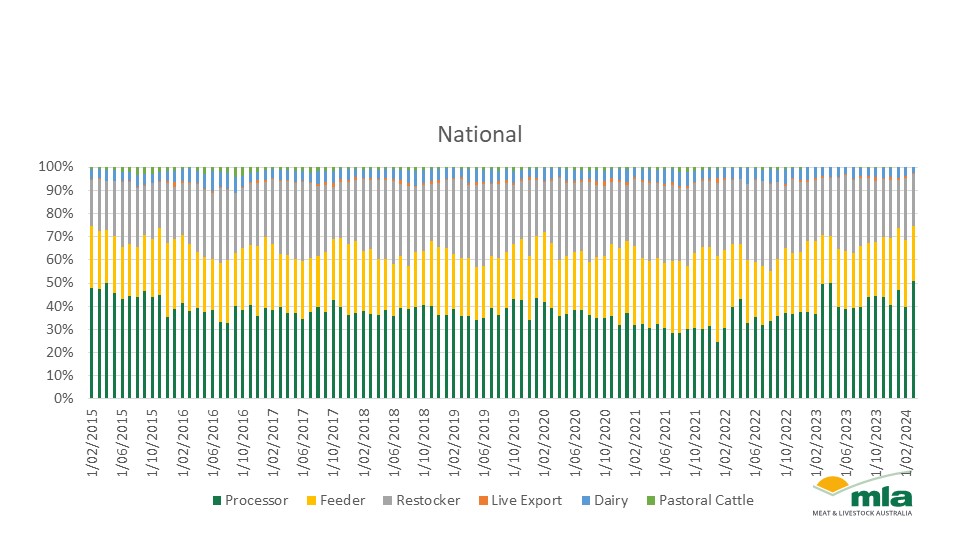

Earlier this month, MLA released the Industry projections 2024: Australian cattle report, citing the herd would ease by less than 1% to 28.6 million head by 30 June 2024. After growing for three consecutive years through the 2020–2022 rebuild, the younger herd has now reached production maturity, pushing more processor-ready animals through sales channels.

Often through rebuilding years, we can see the proportion of cattle sold to processors (green, Figure 1) is lower as high turnoff during liquidation leads to a younger herd. When the herd reaches maturity, processor proportions return to normalcy.

Cattle sold to feedlots (yellow, Figure 1) follow seasonal peaks, which are clearly seen in the charts. Despite these seasonal cycles, when processor-ready cattle sales fall such as during the rebuild of 2020 – 2022, cattle are absorbed into the feedlot sector to be finished on grain to make weight or receive a weight-based premium.

The make-up of cattle sold to processors dropped during the 2020-2022 rebuild, indicating there were fewer processor-ready cattle post the intense destocking that occurred through the 2017–2019 drought years. Proportionally, 2021 was the lowest throughput of processor cattle on record. Looking state by state; 2021 was the smallest processor year for NSW, Queensland and Victoria. In SA and WA, processor cattle proportion fell again in 2022, indicating their rebuild was slightly delayed compared to the rest of the country.

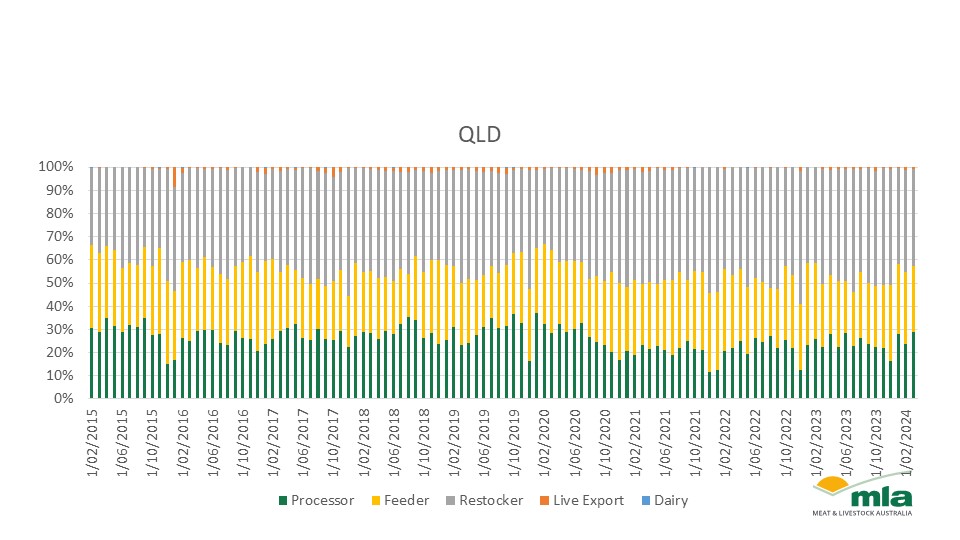

Queensland: growth in feedlot focus

There has been a long-term change in cattle transactions in Queensland saleyards. While we see the seasonal nature of the restocker and processor movements, there has been a longer-term trend of reduced processor cattle sold through saleyards.

This could be due to a number of factors, including:

- new restocker-focused saleyard entering into the National Livestock Reporting System (NLRS)

- producers moving away from end-to-end growth production systems where cattle are born and grown out to processing without being transacted

- growth in direct consignment sales for processor-ready cattle

- feedlot growth in the state has absorbed a proportion of cattle that will be grown out and sold directly to processors.

The number of processor cattle through saleyards hasn’t returned in recent months as it has in other states, supporting the assumption that the northern states are trailing the southern states and remain in a subtle rebuild.

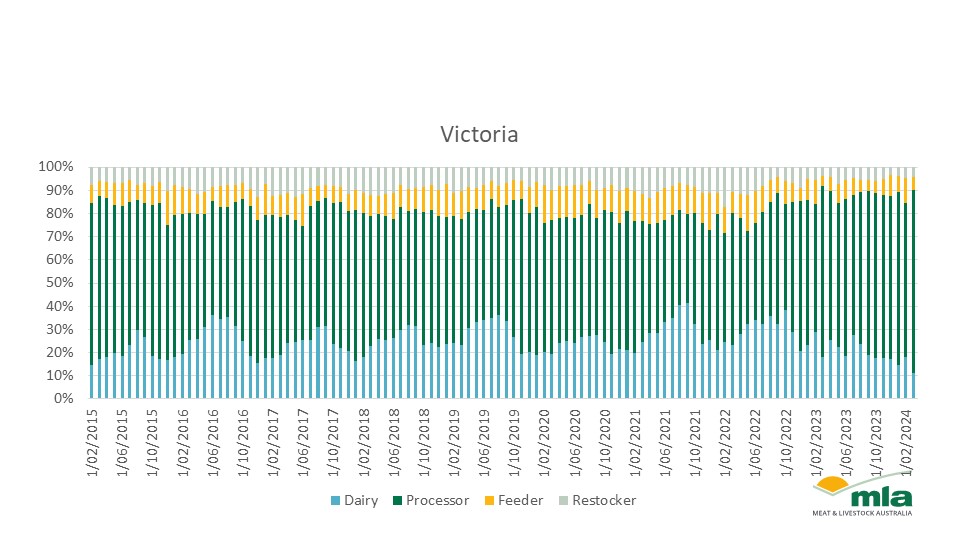

Victoria and the dairy industry

Before 2022, Victoria had very regular seasonal trends in processor cattle sales. These would peak generally from October to March. Since 2022, there has been a shift in the sales type of cattle. Since 2022, dairy cattle (light blue, Figure 3) make-up of sales has eased, indicating a more structural shift in the state away from dairy.

Attribute to: Erin Lukey, MLA Senior Market Information Analyst

{kind=link}