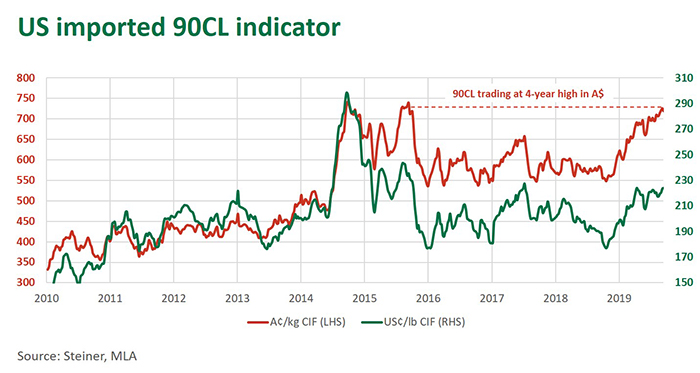

Despite edging lower this week, to 719 A¢/kg CIF (or 224 US¢/lb CIF), the US imported 90CL indicator is trading near a four-year high. Typically when the cow kill in Australia or the US rises, lean manufacturing supplies pickup, keeping a lid on prices. However, a softer A$ and surging demand from China has maintained demand-side pressure and underpinned a 23% rise in the US imported 90CL indicator over the last year.

In the first seven months of 2019, Australian female slaughter – a large part of which has been cull cows – has tracked 17% above year-ago levels and 20% above the five-year average. Comparable figures out of the US show female slaughter tracking 6% above year-ago levels and 24% above the five-year average so far this year.

While beef demand across Asia remains strong, China has added the greatest amount of fuel to the fire over the last twelve months and applied competitive pressure to bids out of the US. The US remains Australia’s largest manufacturing market, accounting for 39% of shipments so far in 2019, however China has recorded the largest swing – two years ago it represented 3% of Australian manufacturing exports but this has grown to 12% in 2019.

However, this also understates the pulling power of China. Depending on price and the quality of cattle coming through, many leg cuts would have traditionally been added to manufacturing combos to the US. However, these hindquarter cuts are now finding willing buyers in the China market. Hindquarter cuts – namely shin shank, knuckles and outside flats – to China have now overtaken forequarter cuts as the largest category, increasing a staggering 81% year-on-year so far in 2019.

Typically, US demand for grinding beef would subside with the end of the summer grilling season. However, a strong US economy, limited supply from New Zealand and competition from Asia has supported imported US pricing (in A$ and US$ terms). Add to that, a recent fire at a major US packer has applied additional buying pressure, as end-users look to secure supply through the remainder of 2019.

These global dynamics have supported Australia cow prices despite seasonal conditions in many regions remaining poor, keeping the cow kill elevated. While cow prices remain below the 500 A¢/kg cwt peak in 2016, with the national medium cow indicator averaging 435 A¢/kg cwt over the last week, they are far better than the 200-300 A¢/kg cwt levels recorded during the 2013-2014 drought.

As US supplies of cow beef increase over coming years with the herd approaching a seasonal peak, rising Asian demand will likely mean Australia manufacturing product will still find a willing buyer. Add to that the additional restocker demand in-waiting of a seasonal break, and significant upside potential for cow prices still remains.

© Meat & Livestock Australia Limited, 2019

To build your own custom report with MLA’s market information tool click here.

To view the specification of the indicators reported by MLA’s National Livestock Reporting Service click here.

{kind=link}