In the U.S., unlike elsewhere in the world, the vast majority of mergers and acquisitions are conducted by “serial acquirers” – large, publicly traded firms that regularly acquire smaller companies. Around four in five M&A deals are made by these major players, including tech titans IBM, Google and Microsoft.

And even the least-successful U.S. acquirers in terms of market reaction will continue to make deals, persisting in spite of less-than-stellar announcement-day returns. This persistence is different from what we see for mergers and acquisitions outside the U.S.

Possible reasons for that distinction: a special focus on technology; the appeal of “intangible assets” in the marketplace; and the strength of governance systems in U.S. financial markets compared to other parts of the world.

“Why is governance so important? Maybe it’s because the system allows you to have poorly performing serial acquirers continue acquiring – it’s sort of a crucible that allows these poor performers to persist longer than they would otherwise,” said Andrew Karolyi, the Charles Field Knight Dean of the Cornell SC Johnson College of Business and a co-author of the study.

Karolyi, also the Harold Bierman, Jr. Distinguished Professor of Management, is senior author of “Why are Serial Acquirers Different in the U.S.?,” published June 11 in Critical Finance Review. His co-authors are Rose C. Liao, associate professor of finance at Rutgers University; and Gilberto Loureiro, professor of finance at the University of Minho in Portugal.

The point of this research, Karolyi said, was to see if the well-studied theories regarding serial merger-and-acquisition activity motivated by evidence in the U.S. also held true elsewhere in the world.

“It’s not surprising that so much capital-markets research focuses on the U.S., because of its size and because of the high concentration of scholars in the U.S. markets,” he said. “That’s fine until you widen the lens, open up to the rest of the world and you find unusual patterns that don’t seem to line up with what’s happening in the U.S., and you either wonder, ‘What’s odd about this other market?’ or you start to wonder whether there’s something special about the U.S. markets. And, if the latter is true, you have to question whether theory should be formulated from the broader evidence.”

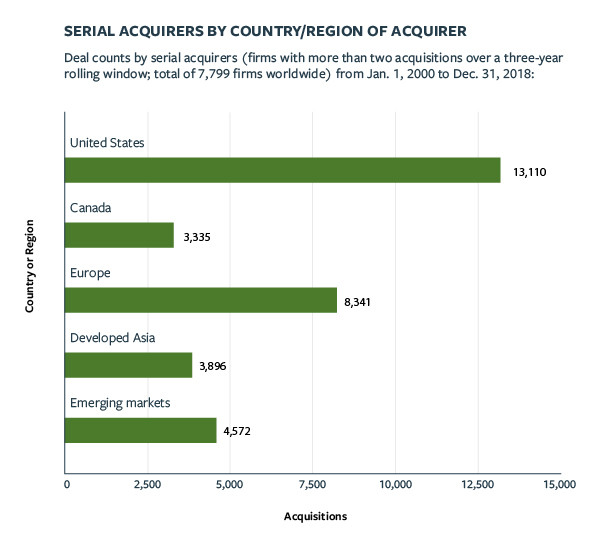

Karolyi and his collaborators analyzed nearly 8,000 serial acquirers around the world that were involved in more than 33,000 domestic and international deals across several decades. The researchers defined “serial acquirers” as those firms acquiring two or more targets in a three-year rolling window. As a starting point, Karolyi and his collaborators used a 2015 study that analyzed U.S. mergers and acquisitions, and which coined the term “extraordinary acquirers” – firms that consistently generate positive returns from their acquisitions.

Using announcement-day returns – the market’s reaction on the days around an acquisition – the researchers found that the top acquirers saw an average increase in the firm’s stock price of around 3.5% following its first acquisition in the three-year window, and persistent returns of more than 3% for each deal over the next five years.

The poorest U.S. acquirers, on the other hand, saw returns of around 1% for the entire five years. This is in contrast to non-U.S. acquirers, where the gap between the extraordinary and extraordinarily-poor acquirers is only about one-third the size of the returns gap in the U.S.

In other words, non-U.S. acquirers that perform poorly aren’t given second – or third, or fourth – chances to prove their mettle, but U.S. firms are.

Karolyi said many factors contribute to this phenomenon. One is the high level of intangible assets, particularly among U.S. tech firms, that make them potentially attractive targets.

“Things like patents, or legal rights to certain licensing arrangements – those are intangible assets,” he said. “And what we know when we compare the U.S. markets to the rest of the world is that U.S. firms, disproportionately, are laden with a larger fraction of their total assets being in intangible form. The U.S. tech industry is sort of a poster child for large intangible asset bases.”

Karolyi sees this research as a jumping-off point for more study into U.S. versus international markets. “We hope this will inspire others to take this bigger, global lens and then pursue other explanations,” he said, “and then maybe we can get come to a really better understanding of this unusual persistence by U.S. serial acquirers.”

Funding support for this work came from the Portuguese Foundation for Science and Technology.

{kind=link}